Effects on the economy

Ghana’s Real GDP growth slowed to 3.3% in 2022, down from 5.4% in 2021 due to the combined effect of macroeconomic instability, global financial tightening, and the lingering impact of the Russia-Ukraine war. The outlook is skewed to the negative due to possible shocks from a prolongment of the war and a tighter global financial market. The World Bank projects the country’s growth to slow further to 1.6 % in 2023 and remain muted in 2024, before returning toward its potential.

The higher MPR set by the MPC is consequently increasing the cost of borrowing for businesses. With higher borrowing costs, businesses might postpone or reduce their investment plans. Projects that were previously economically viable at lower interest rates might become less attractive, leading to a slowdown in capital expenditure. Startups and small businesses, which often rely on external financing, might find it particularly challenging to secure affordable loans. Thus, it may become a challenge for such businesses to invest in new projects and / or expand their operations. This can contribute to and even further slow down economic growth and hinder job creation.

According to the 2022 Report of the Centre for Affordable Housing Finance in Africa, the average loan amount offered by lenders in Ghana, ranges from GH¢80,000 (US$9,930) to GH¢1,600,000 (US$198,650) for cedi mortgages and US$15,000 (GH¢120,815) to US$35,000 (GH¢281,900) for dollar mortgages. In relation to a mean national household income of GH¢2,828 (US$350) per month and a monthly household expenditure of GH¢1,071 (US$133), the affordability of mortgage and housing in general, remains far-fetched.

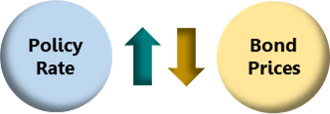

Mortgage rates are closely tied to the prevailing interest rates in the economy. As central banks raise the policy rate, commercial banks adjust their lending rates, causing mortgage rates to rise as well. Higher mortgage rates mean that borrowers will have to pay more in interest over the life of their loans. This can lead to increased monthly mortgage payments, making homeownership more expensive. Thus, a potential reduction on the demand for such mortgages. On the flip side, there could be slower home sales and potentially downward pressure on housing prices. Homeowners with adjustable-rate mortgages or existing mortgages with higher rates might find it less appealing to refinance when rates are higher.

The local currency can also be sensitive to policy rate changes. A higher interest rate in a country can attract foreign investors seeking better returns on their investments. As a result, there might be increased demand for the local currency to invest in financial assets, leading to currency appreciation. All things being equal, a higher rate can encourage foreign capital inflows, as investors seek to take advantage of the higher yields available. This influx of foreign funds can drive up demand for the local currency, leading to its appreciation. The increase can makes financial assets, such as government bonds and other fixed-income instruments, more attractive to investors. This yield advantage can lead to increased demand for the local currency.