According to The Official Monetary and Financial Institutions Forum (OMFIF), an organization that tracks central banking and economic policy, central banks globally recorded losses in a bid to manage their reserves in 2022 amid bond-heavy allocations that took a major hit as a result of aggressive monetary policy tightening around the world and other country-specific factors. According to the OMFIF report, currency interventions in 2022 by monetary authorities to prop up their financial units against a resurgent dollar also contributed to portfolio losses on central bank reserves. The U.S. bond market, the largest in the world for example, had the worst-ever year on record in 2022, undertaking multiple 75 basis-point hikes over the last year to curb stubbornly-high inflation, before decelerating its pace.

Some Central Banks that have recorded losses globally include;

- The Reserve Bank of Australia (RBA) recording a 2022 book loss of 37 billion Australian dollars, which more than wiped out the central bank’s equity.

- The UK Government facing £150 billion bill to cover Bank of England’s losses (According to the Financial Times of July 25, 2023).

- The Swiss National Bank (SNB) in early January reported a record preliminary loss of 132 billion francs for 2022.

- In September 2022, the central bank of the Netherlands notified the country’s government in a letter that it projects net interest losses amounting to a potential EUR 9 billion for the years 2023 through 2026.

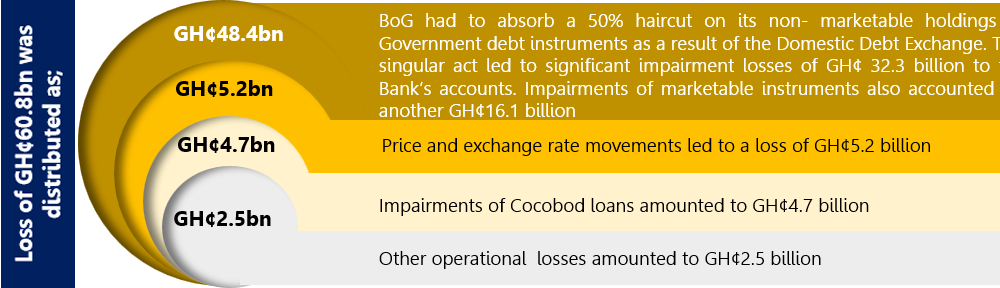

- Ghana’s central bank, unfortunately was not left put of the hit. In its 2022 Annual Report and Financial Statements, The Bank of Ghana (BoG) recorded a loss of GH¢60.8billion having posted a GH¢1.2 billion profit in 2021.

Is it typical for a Central Bank to record looses?

Central banks can report losses especially during seasons of economic downturns. This can be as a result of various factors.

Central banks often hold various assets on their balance sheets, such as government bonds, foreign exchange reserves, and other financial instruments. During economic downturns, the value of these assets can decrease due to market fluctuations, reduced demand, or credit risks. As a result, the central bank may experience losses on the value of its assets.

Central banks may implement certain policies in a bid to stimulate borrowing and spending. Such a policy may be to lower interest rates. When interest rates are lowered, the central bank’s income from its assets, such as government bonds, also decreases. This reduction in income can contribute to losses.

In the face of currency volatility during an economic distress, central banks that hold foreign currency reserves as part of their monetary policy strategy can make losses if the currency depreciates in value relative to its domestic currency.

When a central bank records losses, it can have various implications for banks and the broader economy. The effects depend on the specific circumstances, reasons for the losses, and the actions taken by the central bank in response.

The Case of Ghana’s Central Bank

According to BoG’s 2022 Annual Report and Financial Statements, the loss of GH¢60.8billion is attributed to a decline in the Group’s net worth position due to the impact of the Domestic Debt Exchange Programme (DDEP) and impairment of some assets, which accounted for approximately 88.5% of the loss amount.

BOG steps to recover from loss

It’s important to note that central banks usually aim to manage their operations and respond to challenges in ways that minimize negative impacts on the broader economy and individuals.

In its Annual Report, the Central Bank, outlined these measures as their approach to recovery. These include:

- Retention of profits to help rebuild capital until equity firmly returns to positive region;

- Refrain from monetary financing of the Government of Ghana’s budget. In this respect, action has already been taken with a Memorandum of Understanding on zero financing of the budget signed between the Bank of Ghana and the Ministry of Finance on 26 April, 2023;

- Take immediate steps to optimise the BoG’s investment portfolio and operating cost mix to bolster efficiency and profits; and

- Assess the potential need for recapitalisation support by the government in the medium-to-long term

Ghana’s Central Bank, currently having a negative shareholders’ equity need recapitalisation as a prudential requirement, i.e., improve their balance sheet in order to return to a positive equity position.

What to expect

The effects of central bank losses can be complex and interconnected with broader economic dynamics. The specific implications is dependent on the effectiveness of the central bank’s actions, the economic context, and to some extent, government policies.

If a central bank records losses and local banks are struggling to meet minimum capital requirements, the situation can pose significant challenges for the financial system and the broader economy. The combination of central bank losses and weak banks can create a complex and potentially destabilizing scenario.

Local Banks, who have taken losses and struggling to meet minimum capital or solvency requirements may tend to reduce their lending activities in an attempt to conserve capital. This can lead to a credit contraction, making it difficult for businesses and individuals to obtain loans for investment, consumption, and other essential activities. Reduced lending can ultimately slow down economic growth.

There is the potential for increased market volatility. Asset prices, including stocks, bonds, and other financial instruments, could experience sharp declines due to uncertainty and lack of confidence. The GSE Financial Sector Index is already reflecting this as the index keeps declining on a year-to-date basis.

There is the potential for increased market volatility. Asset prices, including stocks, bonds, and other financial instruments, could experience sharp declines due to uncertainty and lack of confidence. The GSE Financial Sector Index is already reflecting this as the index keeps declining on a year-to-date basis.

It is expected that there will be a close coordination between regulatory authorities, the central bank, and the government. Effective coordination is necessary to restore confidence, stabilize the financial system, and implement appropriate policy measures.

To address these challenges, governments, central banks, and regulatory authorities would need to implement a combination of monetary, fiscal, and regulatory measures. These might include capital injections, liquidity support, recapitalization of banks, policy adjustments, and efforts to restore market confidence. The aim would be to stabilize the financial system, restore trust, and prevent further deterioration of economic conditions.

Considering the huge negative equity position, until the Central Bank of Ghana has moved into positive equity regions, one questions whether the BoG has the moral right to revoke the license of any Bank that lacks sufficient capital.

Given the current high inflation rate in the country and year end target of 38.1%, it is important that the Central Bank refrain from further deficit financing on the Government in order to strengthen its money market operations and also demonstrate that even with a negative equity position, it can sustain the economy adequately.

—————————————————————————————————————————————————————————————-

The information contained in this blog is being provided for educational purposes only and does not constitute a recommendation from any Bora Capital Advisors entity to the recipient. Bora Capital Advisors is not providing any financial, economic, legal, investment, accounting, or tax advice through this blog to its recipient.

This report reflects the views and opinions of Bora Capital Advisors Ltd, and is provided for information purposes only. Although the information provided in the market review and outlook section is, to the best of our knowledge and belief correct, Bora Capital Advisors Ltd, its directors, employees and related parties accept no liability or responsibility for any loss, damage, claim or expense suffered or incurred by any party as a result of reliance on the information provided and opinions expressed in this report, except as required by law. The portfolio performance data represented in this report represents past performance and does not guarantee future performance or results.