As 2026 unfolds, the Ghanaian economy is showing clear signs of macroeconomic stabilization

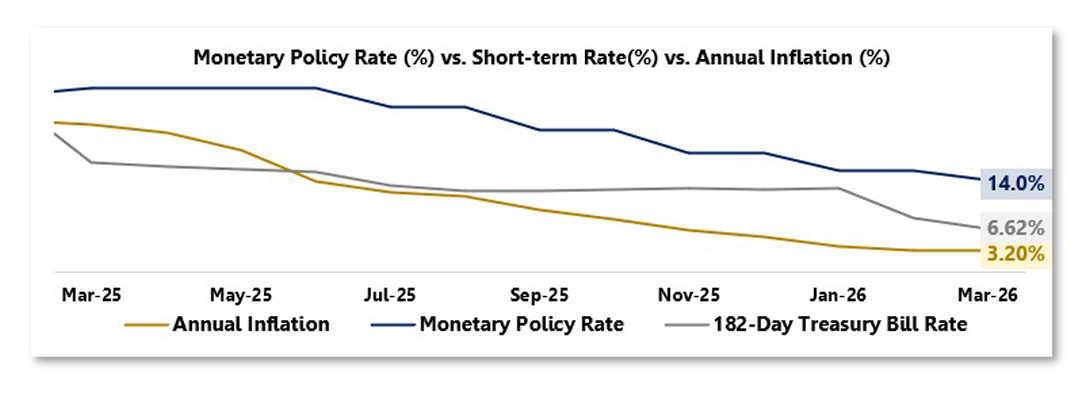

By February, inflation had dropped to 3.3%, extending a fourteen-month disinflation trend from 23.5% in January 2025. Over the same period, the Bank of Ghana reduced the Monetary Policy Rate (MPR) from 18.0% to 15.50%, before a further cut to 14.0% in March, bringing cumulative easing in 2026 alone to 400 basis points. This policy shift reflects improving macroeconomic fundamentals and declining price pressures.

While lower policy rates enhance liquidity and reduce borrowing costs across the economy, they also fundamentally reshape investment dynamics. As risk-free returns compress, investors are increasingly pushed along the risk curve in search of yield. In this environment, the opportunity set expands, but so do the stakes.

The Downward Trend in Treasury Bill Yields

The easing cycle is rapidly repricing Ghana’s Treasury bill market. At the start of 2025, short-term government securities delivered outsized returns, with the 182-day bill yielding above 28%. That window has now closed, and demand dynamics tell the story.

February auctions were heavily oversubscribed by 201.4%, but by March, oversubscription had dropped to just 14.0% as investors began rotating into more competitive opportunities. By the final auction of March 2026, the market turned undersubscribed by 20.14%: a clear signal that prevailing yields are no longer compelling.

For conservative investors, the implication is clear: the era of easy, high risk-free returns is ending. In this environment, attention is gradually shifting toward equities as a more viable source of return.

Equities as the New Return Engine

As fixed income yields compress, capital is rotating into equities in search of higher returns. As Treasury bill yields decline, equities become relatively more attractive, particularly dividend-paying and large-cap stocks capable of delivering positive real returns in a low-inflation environment.

However, this shift also brings greater exposure to market volatility, earnings uncertainty, and potential mispricing. The key question, then, is: How should investors position themselves to navigate this new landscape?

Strategic Positioning in a Lower Rate Environment

The changing rate landscape requires a more deliberate and diversified investment approach:

- Selective Equity Allocation

Equities present a compelling avenue for long-term wealth creation, but selectivity is critical. Investors should focus on fundamentally strong companies with strong earnings potential, sound balance sheets, and consistent dividend profiles.

- Diversification as a Core Strategy

Portfolio diversification is increasingly essential. Allocating across asset classes, sectors, and maturities can help mitigate downside risk while enhancing return potential. A clearly defined investment objective, risk tolerance, and time horizon remain central to effective portfolio construction.

- Exploring Alternative Fixed Income Options

Given a low-interest rate environment, it becomes crucial to explore alternative fixed income instruments such as corporate issuances, commercial paper, and fixed deposits to serve a similar purpose. These instruments can offer competitive yields, portfolio diversification, and improved risk-adjusted returns, although they may come with varying levels of credit and liquidity risk that require careful assessment.

Declining interest rates have reshaped Ghana’s securities market by compressing bond yields, driving capital into equities, and altering investor behavior. While the easing cycle has created opportunities for capital appreciation, it has also increased the consequences of poor allocation decisions.

In a lower-rate environment, the margin for error narrows. Investors who adopt disciplined, well-diversified strategies will be better positioned to preserve real returns and capitalize on opportunities within Ghana’s evolving financial landscape.

——————————————————————————————————————————————————————————————————————————-

The information contained in this blog is being provided for educational purposes only and does not constitute a recommendation from any Bora Capital Advisors entity to the recipient. Bora Capital Advisors is not providing any financial, economic, legal, investment, accounting, or tax advice through this blog to its recipient.

This report reflects the views and opinions of Bora Capital Advisors Ltd, and is provided for information purposes only. Although the information provided in the market review and outlook section is, to the best of our knowledge and belief correct, Bora Capital Advisors Ltd, its directors, employees and related parties accept no liability or responsibility for any loss, damage, claim or expense suffered or incurred by any party as a result of reliance on the information provided and opinions expressed in this report, except as required by law. The portfolio performance data represented in this report represents past performance and does not guarantee future performance or results.