For over a century, the most reliable path to building wealth in financial markets has not been speed, speculation, or brilliance, but discipline.

Investors who commit to making steady investment contributions, long-term planning, and disciplined strategies have generally achieved more reliable investment results than people who chase short-term trends. This philosophy was championed by John Bogle, who promoted inexpensive index fund investing. He also advocated for long term investing, no matter the fluctuations in the short term, rather than trying to beat the market. There were many people who made mockery of John Bogle when he established the Vanguard Group in 1975 and introduced the first index fund for regular investors. It was referred to as “Bogle’s Folly.” And why? Because Bogle made it his goal to meet the market, at a minimal cost, rather than to beat it. Nearly sixty years later, trillions of dollars have been invested in index funds, and his philosophy has aided millions of investors in accumulating long-term wealth. So, what exactly makes this approach so powerful? Why has it worked through some of the most turbulent financial periods in modern history? The answer is simple: compounding!

The Power of Compounding

At its core, long-term investing is about compounding. It is basically your money having babies, and those babies having more babies. Over time, that growth turns into a massive snowball. An example is the S&P 500, which has historically delivered average annual returns of roughly 9–10% over long periods, including reinvested dividends. While individual years may swing dramatically, decades of steady participation have rewarded patient investors. What makes this powerful is not dramatic spikes, but consistency. A modest investment, left to grow over decades, can multiply significantly. When combined with regular contributions, the effect becomes even more pronounced. Compounding does not demand brilliance; it requires patience.

Diversification

But growth alone is not enough; you also need to protect what you’re building. That’s where diversification comes in. While compounding drives long-term returns, diversification helps manage the risks that come with staying invested over time. By spreading investments across different asset classes and industries, investors reduce the impact of any single underperforming asset. In simple terms, you’re not putting all your eggs in one basket. This makes the overall portfolio more resilient, as different assets tend to respond differently to economic conditions.

Staying the Course Even in Crisis

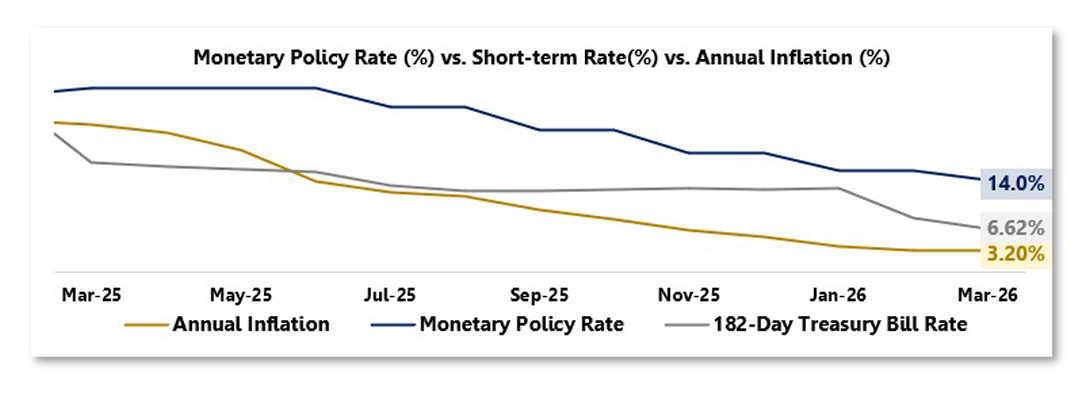

Even with a well-diversified portfolio, the greatest challenge in investing often lies not in strategy but in behavior—behavioral biases. Patience becomes most difficult and most critical during periods of uncertainty. A recent Ghanaian example is the Domestic Debt Exchange Programme in 2022. The announcement sparked significant anxiety among bondholders, prompting many to exit positions at steep discounts to avoid potential losses. As the process progressed and clarity improved, conditions stabilized. Investors who stayed the course were generally better positioned than those who sold early and crystallized losses. The pattern is consistent: in periods of stress, fear drives premature decisions, while patience supports long-term value preservation.

The Risk of Chasing Trends

Short-term speculation can be tempting, but it often comes at a cost. In 2018, Ghana experienced the collapse of Menzgold Ghana Limited, which had attracted investors with promises of unusually high returns. Many concentrated their funds in the scheme, drawn by its apparent consistency. When operations were halted by the Securities and Exchange Commission Ghana, investors lost access to their funds, with those most exposed bearing the greatest losses. In contrast, diversified portfolios proved more resilient. Chasing “hot” opportunities may seem attractive, but diversification remains the more reliable safeguard.

Investing Is a Marathon, not a Sprint

The metaphor holds true: investing is a marathon. A sprinter might look impressive for the first hundred meters, but endurance is what wins a marathon race. Equity markets globally have endured numerous financial crises, recessions, and geopolitical tensions. Yet long-term trends have remained upward. It is not to say that markets are risk-free; they are not. The lesson is that time, diversification, and discipline reduce risk and enhance opportunity.

Successful investing is less about predicting the future and more about preparing for it. By focusing on consistency, embracing diversification, and maintaining discipline through market cycles, investors can harness the full power of long-term growth. For many, consulting an investment advisor adds another layer of structure, helping investors align investment decisions with long-term goals and risk tolerance, manage risks, and seize opportunities aligned with their goals.

——————————————————————————————————————————————————————————————————————————-

The information contained in this blog is being provided for educational purposes only and does not constitute a recommendation from any Bora Capital Advisors entity to the recipient. Bora Capital Advisors is not providing any financial, economic, legal, investment, accounting, or tax advice through this blog to its recipient.

This report reflects the views and opinions of Bora Capital Advisors Ltd, and is provided for information purposes only. Although the information provided in the market review and outlook section is, to the best of our knowledge and belief correct, Bora Capital Advisors Ltd, its directors, employees and related parties accept no liability or responsibility for any loss, damage, claim or expense suffered or incurred by any party as a result of reliance on the information provided and opinions expressed in this report, except as required by law. The portfolio performance data represented in this report represents past performance and does not guarantee future performance or results.