BOG steps to recover from loss

It’s important to note that central banks usually aim to manage their operations and respond to challenges in ways that minimize negative impacts on the broader economy and individuals.

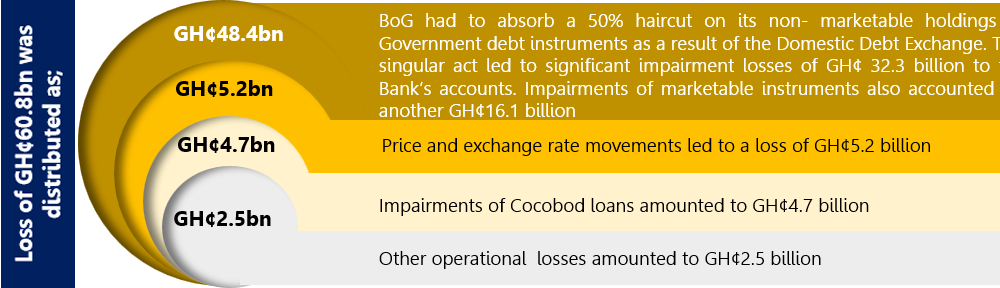

In its Annual Report, the Central Bank, outlined these measures as their approach to recovery. These include:

- Retention of profits to help rebuild capital until equity firmly returns to positive region;

- Refrain from monetary financing of the Government of Ghana’s budget. In this respect, action has already been taken with a Memorandum of Understanding on zero financing of the budget signed between the Bank of Ghana and the Ministry of Finance on 26 April, 2023;

- Take immediate steps to optimise the BoG’s investment portfolio and operating cost mix to bolster efficiency and profits; and

- Assess the potential need for recapitalisation support by the government in the medium-to-long term

Ghana’s Central Bank, currently having a negative shareholders’ equity need recapitalisation as a prudential requirement, i.e., improve their balance sheet in order to return to a positive equity position.

What to expect

The effects of central bank losses can be complex and interconnected with broader economic dynamics. The specific implications is dependent on the effectiveness of the central bank’s actions, the economic context, and to some extent, government policies.

If a central bank records losses and local banks are struggling to meet minimum capital requirements, the situation can pose significant challenges for the financial system and the broader economy. The combination of central bank losses and weak banks can create a complex and potentially destabilizing scenario.

Local Banks, who have taken losses and struggling to meet minimum capital or solvency requirements may tend to reduce their lending activities in an attempt to conserve capital. This can lead to a credit contraction, making it difficult for businesses and individuals to obtain loans for investment, consumption, and other essential activities. Reduced lending can ultimately slow down economic growth.

There is the potential for increased market volatility. Asset prices, including stocks, bonds, and other financial instruments, could experience sharp declines due to uncertainty and lack of confidence. The GSE Financial Sector Index is already reflecting this as the index keeps declining on a year-to-date basis.

There is the potential for increased market volatility. Asset prices, including stocks, bonds, and other financial instruments, could experience sharp declines due to uncertainty and lack of confidence. The GSE Financial Sector Index is already reflecting this as the index keeps declining on a year-to-date basis.

It is expected that there will be a close coordination between regulatory authorities, the central bank, and the government. Effective coordination is necessary to restore confidence, stabilize the financial system, and implement appropriate policy measures.

To address these challenges, governments, central banks, and regulatory authorities would need to implement a combination of monetary, fiscal, and regulatory measures. These might include capital injections, liquidity support, recapitalization of banks, policy adjustments, and efforts to restore market confidence. The aim would be to stabilize the financial system, restore trust, and prevent further deterioration of economic conditions.

Considering the huge negative equity position, until the Central Bank of Ghana has moved into positive equity regions, one questions whether the BoG has the moral right to revoke the license of any Bank that lacks sufficient capital.

Given the current high inflation rate in the country and year end target of 38.1%, it is important that the Central Bank refrain from further deficit financing on the Government in order to strengthen its money market operations and also demonstrate that even with a negative equity position, it can sustain the economy adequately.